Third Wave Carbon is committed to accelerating carbon neutrality via education, fostering community & developing environmentally responsible, low-cost energy assets.

Investing in clean Energy for Today,

Tomorrow and our Future

Third Wave Carbon’s mission is to educate businesses, Governments & humans on innovative methods to deploy clean energy technologies so that we all may leave a cleaner planet for our children and our childrens children…

The modern carbon market was born out of the Kyoto protocol in 1997 which outlined international climate agreements that created tradeable emissions reductions.

In 2015 the Paris accord ushered in the corporate net zero era which saw corporations begin to commit to net zero emmissions. Over 1100 companies have pledged net-zero goals by mid 2020’s…

Carbon markets are developing as a crucial economic lever in the challenge of reversing the accumulation of greenhouse gases in the Earth’s atmosphere, while CO2 remains a key factor in a range of industrial sectors.

National governments are embracing carbon markets, with a proliferation of carbon pricing policies worldwide. The private sector is channelling finance into projects that generate carbon emissions reductions and removals to mitigate their hard-to-abate emissions.

And the United Nations is making progress in building a global marketplace for carbon emissions reductions that will facilitate nations’ attempts to meet their obligations under the Paris Agreement.

Industrial sectors remain a key source of CO2 emissions and consumption, with innovation looking towards sustainable methods of production and utilisation.

The world must remove 5–16 billion metric tons of CO₂ annually by 2050 to limit global warming to 1.5°C.

Carbon dioxide removal includes technologies and natural methods that capture and store CO₂ from the air. CDR is crucial for achieving global climate goals, as reducing emissions alone is not enough to limit global warming.

CDR credits let companies and governments balance their emissions. They do this by funding projects that actively remove CO₂. CDR credits are different from traditional carbon offsets.

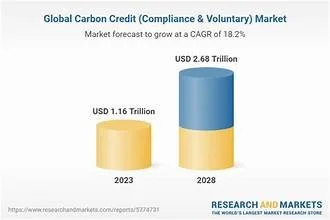

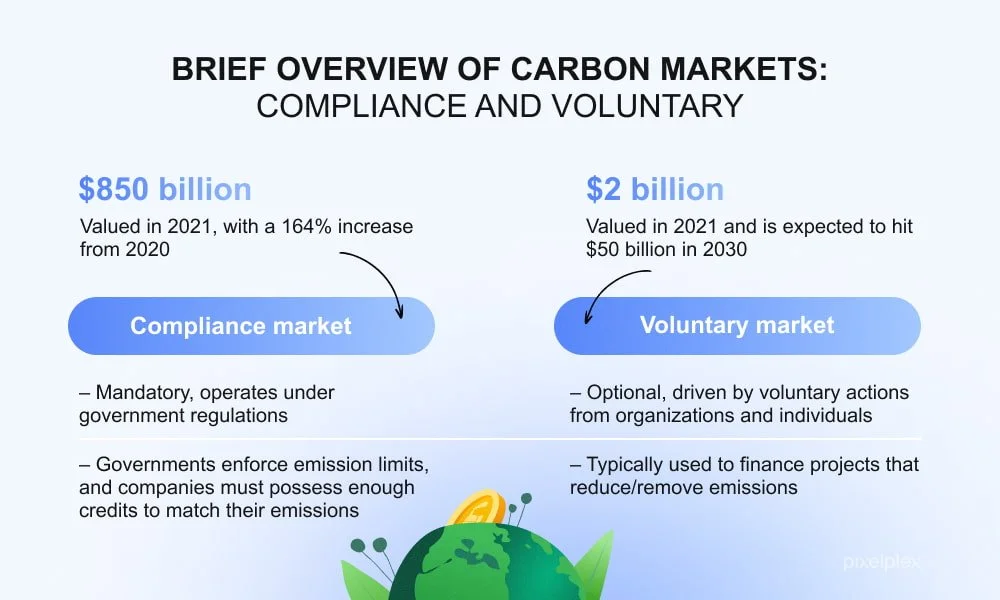

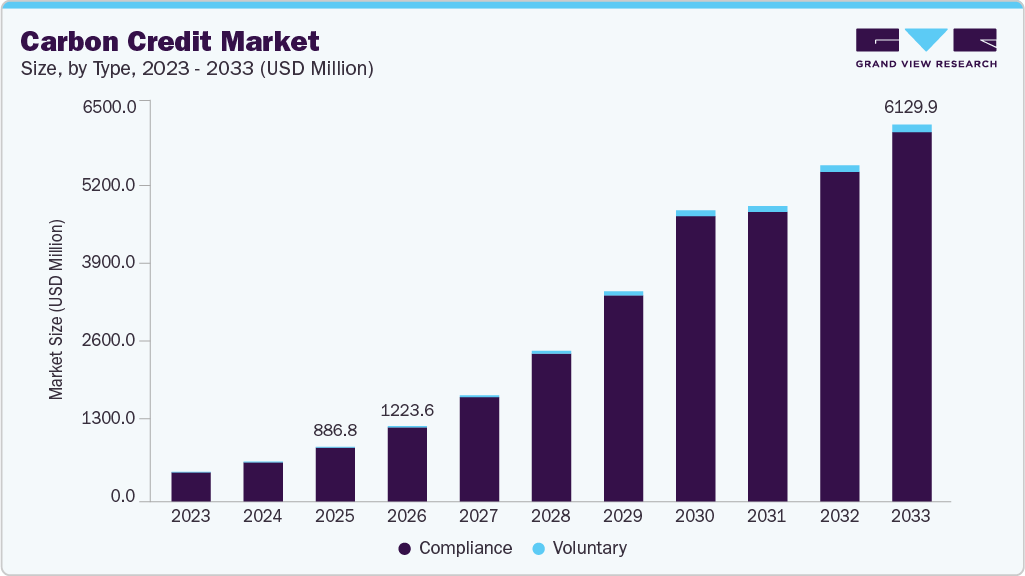

While carbon offsets aim to reduce or avoid emissions, like stopping deforestation, CDR credits guarantee that CO₂ is pulled out of the air and stored for a long time. The voluntary carbon market (VCM) is expected to grow from $2 billion in 2023 to over $50 billion by 2030, with CDR credits playing a significant role.

How Does CDR Work? The Science Behind Carbon Removal

CDR captures CO₂ from the air. It then stores it permanently in geological formations, biomass, or other stable places. There are two main types of CDR methods:

Natural CDR: Includes afforestation, soil carbon sequestration, and ocean-based methods.

Technological CDR: Includes Direct Air Capture (DAC), biochar, and enhanced mineralization.

Permanence is key in carbon dioxide removal. High-quality CDR credits must keep CO₂ stored for centuries or even millennia. This prevents it from being released back into the atmosphere.

Recent research shows that engineered carbon removal solutions like DAC can store carbon for over 1,000 years. This makes them very effective for long-term carbon management.

Several global projects are currently implementing these solutions. In Iceland, the Orca plant by Climeworks is the largest DAC facility, capturing 4,000 metric tons of CO₂ per year, with plans to scale to 1 million tons annually by 2030.

In the U.S., the Department of Energy has committed over $3.5 billion to support DAC projects under the Regional DAC Hubs initiative.

Who Buys Carbon Removal Credits and Why?

The CDR market is growing fast. Corporate buyers, governments, and voluntary markets are boosting demand.

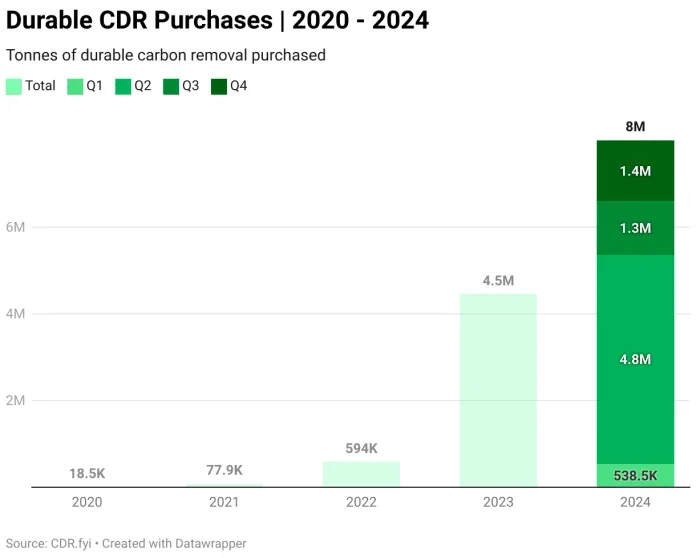

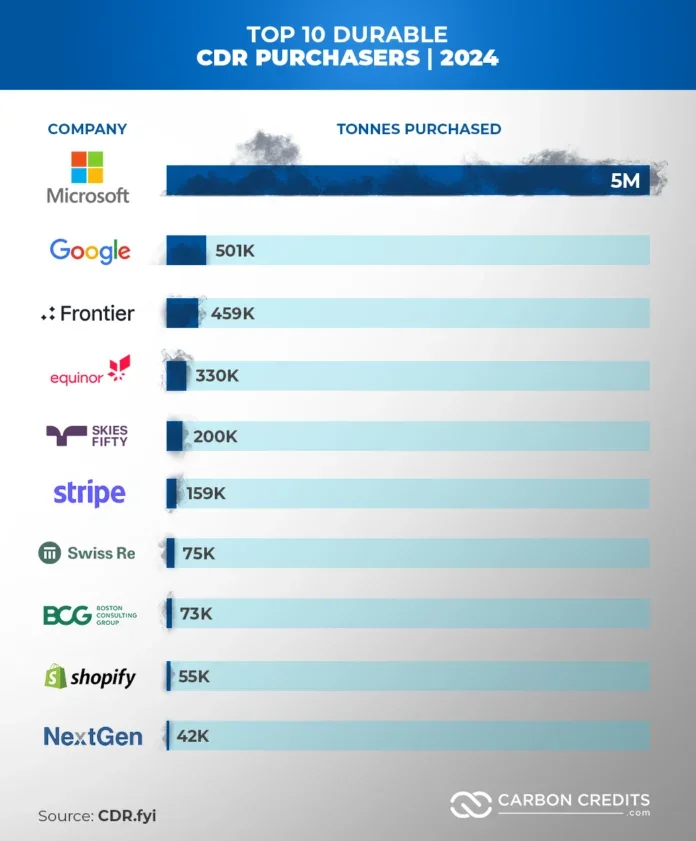

In 2024, purchases of high-durability CDR credits reached almost 8 million metric tons, compared to 4.5 million metric tons in 2023 as shown in the chart. This represents an increase of approximately 78% year-over-year, according to the CDR.fyi report.

Key players in the market include:

Microsoft accounted for 63% of total CDR purchase volume in 2024 to achieve carbon negativity by 2030. The tech giant secured around 5.1 million metric tons of durable CDR credits.

Google purchased about 501 thousand tons of CDR credits, making it second to Microsoft.

Frontier buyers—including Stripe, Shopify, and Watershed—continued to support promising carbon removal projects, collectively purchasing 667.4K tonnes of CDR credits.

This isn’t just a business—it’s a reflection of what we believe in. We’re here to collaborate with disparate stakeholders to create work that matters, yielding lasting results led by a shared commitment to quality and care for the world environment .

Big Ideas, Real Impact

The landscape for carbon credits and removals in 2026-2027 is undergoing a major shift toward high-integrity compliance, driven by the tightening regulations of the aviation sector's CORSIA scheme and the evolution of voluntary, high-quality removal opportunities in higher education.

Here is an explanation of the upcoming opportunities pipelines.

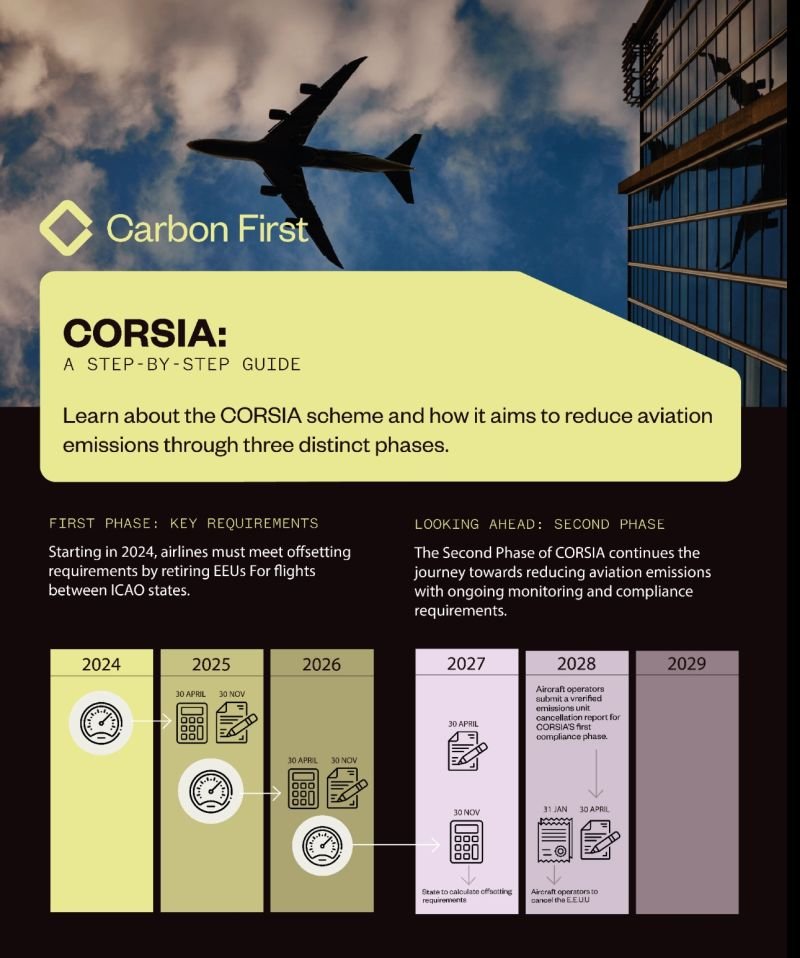

1. CORSIA: The Mandatory Aviation Pipeline (2026-2027+)

CORSIA (Carbon Offsetting and Reduction Scheme for International Aviation) is the first global compliance scheme for a specific sector. It requires airlines to offset emissions above 85% of 2019 levels.

Phase 1 (2024–2026): Voluntary participation, with 130 states participating as of January 2026. This phase focuses on establishing MRV (Monitoring, Reporting, and Verification) and initial procurement.

Phase 2 (2027–2035): Participation becomes mandatory for most nations, including major aviation markets like China, Brazil, and India.

The Opportunity Pipeline (2026-2027):

High-Integrity Units Needed: Demand is expected to outstrip supply, particularly for CORSIA-eligible units (CEEUs) authorized under Article 6 of the Paris Agreement (to avoid double counting).

Approved Standards: Only specific standards (e.g., American Carbon Registry, ART TREES, Gold Standard) are permitted.

Shift to Removals: While reduction projects currently dominate, CORSIA is expected to increasingly favor high-permanence removals, with demand projected to rise significantly by 2027.

2026 Milestones: March 2026 saw the first large-scale retirement of CORSIA-eligible credits by a commercial airline, signaling the move from policy design to operational implementation.

2. Higher Education Carbon Credit Pipelines (2026-2027)

Universities are transitioning from being just voluntary offset buyers to developers of high-quality removal and reduction projects.

C2P2 (Carbon Credit and Purchasing Program): Managed by Second Nature, this initiative supports colleges in developing verified carbon offsets on their campuses through energy efficiency, renewable energy, and LEED building projects.

Refrigerant Destruction (High-Impact Opportunity): Higher education institutions are partnering with firms like Tradewater to identify and destroy old refrigerants (CFCs/HCFCs) on campus, generating high-value, immediate-impact carbon credits.

Student-Led Innovation & Research:

OpenAir Carbon Removal Challenge: A global competition focusing on developing new, scalable Carbon Dioxide Removal (CDR) technologies, with winners presenting at high-level industry events.

Integrity Focus: Academic institutions (e.g., Berkeley Carbon Trading Project) are leading the development of research-backed frameworks to ensure the integrity of carbon markets, providing guidance for ethical purchasing.

2026/2027 Outlook:

Increased Sophistication: Schools are moving toward forward-purchasing agreements and on-campus projects that offer higher additionality and lower reputational risk compared to legacy forestry projects.

Focus on Local Impact: Increased investment in sustainability projects on campus using proceeds from credit sales (C2P2 model).

Summary of Future Trends

Feature

CORSIA (2026-2027)Higher Education Pipelines (2026-2027)DriverRegulatory Compliance (UN/ICAO)Net-Zero Goals & Student ActionKey DemandHigh-integrity, Article 6 alignedHigh-quality removals/AvoidanceProject TypesART TREES, Cookstoves, New DACCSRefrigerants, Energy Efficiency, CDR2026-27 FocusSupply Crunch, 2027 Mandatory StageOn-campus, Verified, Transparent

Note: In 2026, the voluntary carbon market faces a "critical inflection point" with a high demand for carbon dioxide removal (CDR) but low current supply of high-durability projects.

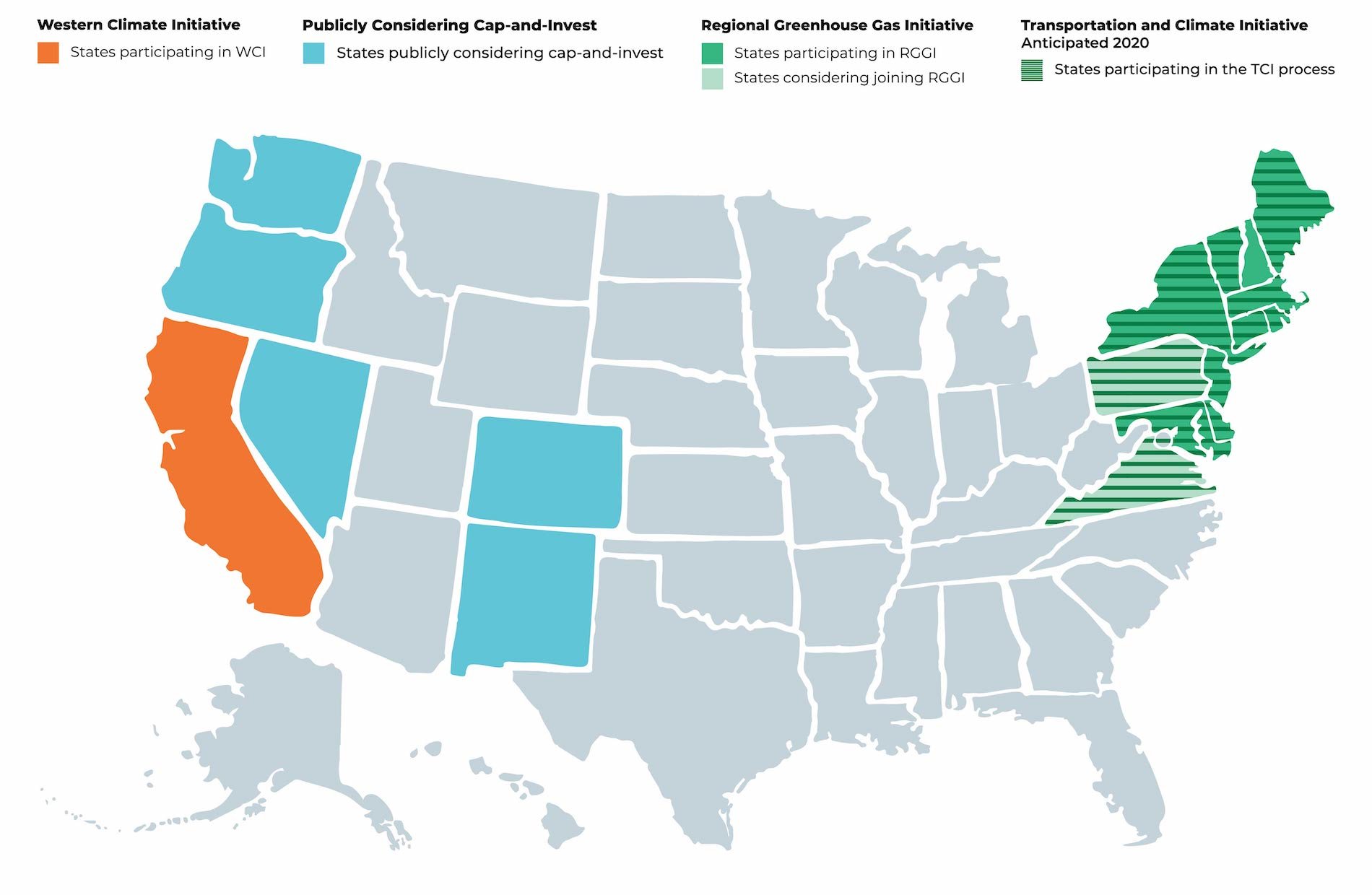

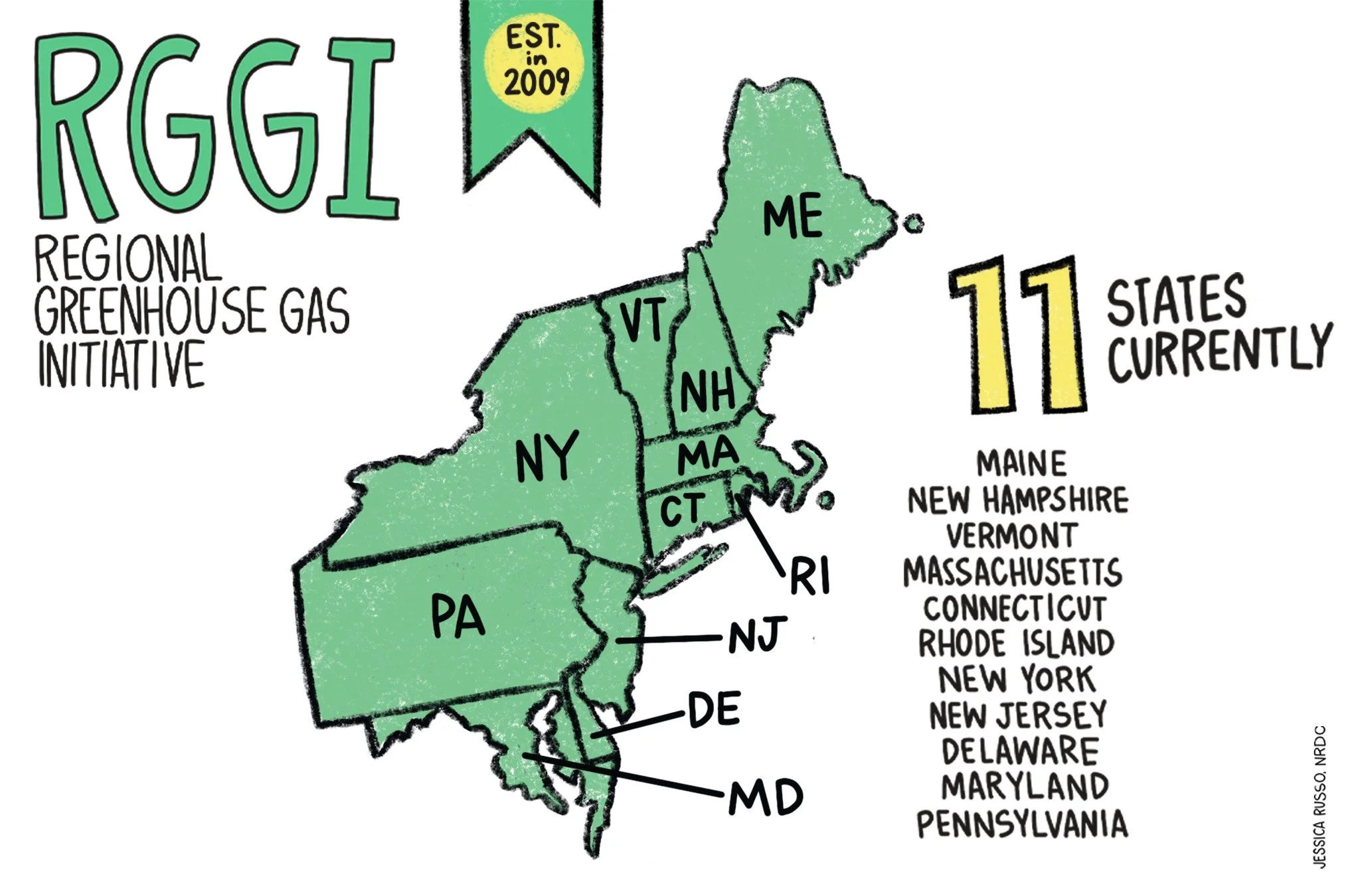

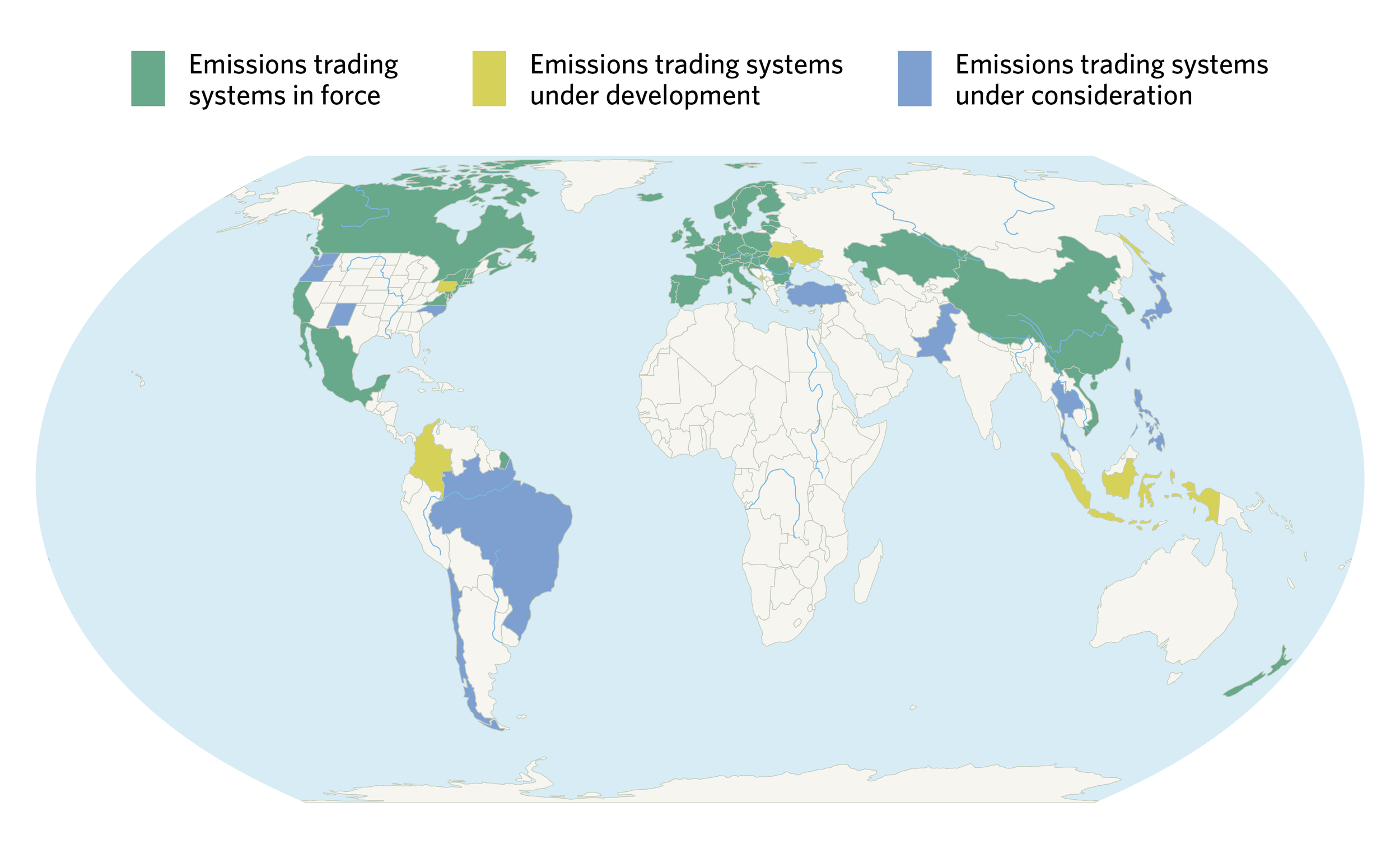

Most states in the US are entirely voluntary markets at present; see the details on state based regulation via RGGI (REgional Greenhouse Gas Inititive) in the East and Also Cap & TRade in California which do offer frameworks at the state level:

The United States utilizes market-based carbon regulatory schemes to reduce greenhouse gas (GHG) emissions, primarily through Cap-and-Trade systems. These programs set a limit ("cap") on total emissions and require companies to hold allowances for their pollution, allowing them to buy or sell these permits ("trade") in a market.

The most prominent example in the U.S. is the Regional Greenhouse Gas Initiative (RGGI), which is specifically tailored to the power sector.

1. RGGI (Regional Greenhouse Gas Initiative)

Launched in 2009, RGGI is the first mandatory, market-based cap-and-invest program in the United States, covering emissions from the power sector in the Northeast and Mid-Atlantic regions.

Participants (As of early 2026): Connecticut, Delaware, Maine, Maryland, Massachusetts, New Hampshire, New Jersey, New York, Rhode Island, and Vermont.

Scope: Regulates CO2 emissions from fossil-fuel-fired electric power plants with a capacity of 25 megawatts (MW) or greater.

How it Works (Cap-and-Invest):

The Cap: States set a regional budget (cap) on CO2 allowances, which declines over time. The cap is designed to reduce emissions 30% below 2020 levels by 2030.

Allowances: Regulated power plants must hold allowances equal to their total CO2 emissions over a three-year control period.

Auctions: Over 90% of allowances are sold through quarterly, regional auctions.

Proceeds/Investment: Auction proceeds are returned to the states and primarily invested in consumer benefit programs, such as energy efficiency, renewable energy, and direct bill assistance.

Market Stability:

Cost Containment Reserve (CCR): A reserve of allowances released if prices exceed set levels (e.g., $18.22 in 2026), preventing excessive price spikes.

Emissions Containment Reserve (ECR): Allowances are withheld if prices fall below a certain trigger (e.g., $8.41 in 2026), forcing further emissions reductions if the market is oversupplied.

2026–2027 Outlook: Following the Third Program Review concluded in 2025, RGGI states are updating regulations to tighten the cap further starting in 2027, including stronger ECR/CCR mechanisms.

2. Cap-and-Trade (General Concept & Other U.S. Systems)

Cap-and-trade is a policy tool that allows the market to determine the cost of emissions, rather than a government-mandated technology standard.

Mechanism: The government issues a limited number of allowances. Companies can trade allowances, rewarding those that reduce emissions efficiently and creating a financial penalty for those that do not.

Key Design Elements:

Declining Cap: The total allowable emissions decrease annually.

Banking: Unused allowances can be saved for future compliance periods.

Offsets: Some programs allow companies to use credits from projects that reduce emissions outside the covered sectors (e.g., forestry).

Other U.S. Systems:

California Cap-and-Trade: A broad, economy-wide program (launched 2013) covering 80% of the state’s emissions, including transportation fuels and industry. It is linked with Quebec.

Washington State Cap-and-Invest: An economy-wide program targeting large emitters that began in 2023, aiming for net-zero by 2050.

New York Cap-and-Invest: New York is preparing an economy-wide program to complement or eventually replace its RGGI participation.

Key Differences

RGGI is a focused program covering only the power sector across multiple states, while California and Washington operate broad, economy-wide systems designed to reduce emissions across all economic sectors.

Airline carrier INDUstry is moving from a VOluntary to compliance market globally per the paris accord!

USA REgulatory outlook is a game changer!

BIG PICTURE: TWO NEW LAWS RESHAPING DIGITAL FINANCE, PROVIDING A UNIQUE OPPORTUNITY FOR THE CARBON MARKETS

Two new U.S. laws—the Genius Act and the Clarity Act—bring clarity and structure to how digital financial assets are regulated:

- Genius Act: Focuses on stablecoins (digital currencies tied to a stable value like the U.S. dollar) and protocol tokens (used in platforms like Ethereum).

- Clarity Act: Goes further—defining roles for digital asset brokers, dealers, and key regulators like the SEC (Securities and Exchange Commission) and CFTC (Commodity Futures Trading Commission).

WHY IT MATTERS: For the first time, digital assets can be regulated like other financial assets, giving them legitimacy and allowing financial institutions to handle them.

CARBON CREDITS: From “Stranded Assets” to Financial Powerhouses

What Are Carbon Credits?

- Carbon credits are proof that a company helped reduce CO₂ emissions. Today, they are mostly unregulated and can’t be held by banks or used in structured finance.

CURRENT ISSUES AND PAIN POINTS:

- No transparency or standardization

- Can’t be audited or verified easily

- Not accepted by traditional finance (they’re like cash you can’t deposit)

WHAT'S CHANGING?

UNDER THE NEW LAWS:

- Carbon credits can be turned into regulated digital assets AKA RWA’s or Real World Assets.

- Financial institutions like banks, trust companies, and brokers can now custody (legally hold) them.

- This means they can be used for collateral, loans, and investment products—just like other financial assets.

BUSINESS IMPACT: BUY, HOLD, PROFIT

- OLD MODEL: “Buy and Retire”: Companies buy carbon credits and write them off as an expense (COGS – cost of goods sold). This reduces earnings.

- NEW MODEL: “Buy and Bank”: Now, companies can: Add carbon credits to their balance sheet (like prepaid inventory), Treat them as valuable assets that might appreciate over time, Manage risk (just like fuel hedging in airlines), Increase market demand and value, This shift turns carbon credits into a mainstream financial asset class, attracting institutional investors.

THIRD WAVE’S UNIQUE ADVANTAGE

Regulatory Footprint:

- Third Wave is one of the first companies legally allowed to issue and sell digital assets.

- Registered in Bermuda, a global leader in climate risk finance (known for “CAT Bonds”).

Technology & IP:

- Strategic partners with IP holdings consisting of patents to connect raw data from devices (IoT, sensors, etc.) directly to financial assets using smart contracts.

- This allows real-time tracking, auditability, and risk reporting for things like:

Carbon credits

- Renewable energy credits (RECs)

- Sustainability-linked loans and bonds

Real-World Examples:

- Working with the Brazil Central Bank, MERCOSUR AKA The Southern Common Market a South American trade bloc established by the Treaty of Asunción in 1991 and Protocol of Ouro Preto in 1994. Its full members are Argentina, Bolivia, Brazil, Paraguay, and Uruguay. Venezuela is a full member but has been suspended since 1 December 2016. Chile, Colombia, Ecuador, Guyana, Panama, Peru, and Suriname are associate countries, NU Bank Brazil’s largest next gen financial institution & Farm Credit bureau.

- Offering automated settlement, micro-transactions, pooled carbon, and Scope 3 emissions reporting.

FINAL TAKEAWAYS:

- Thanks to these new laws, carbon credits are no longer just good deeds—they’re financial tools. The Carbon Credit conversation is now a CFO level conversation while previously it was a engineering or ecological mid level employee designated talk.

See below for a global glance at Voluntary VS. Compliance territory across the world. Average fine/penalty for non compliance is approx. 3X the credits required under the scheme so treble damages essentially apply in numerous jurisdictions.

Carbon is the building Block of the future!!

Third Wave Carbon offers a full suite of carbon solutions that can help you navigate carbon markets, manage your carbon risks and opportunities, develop and implement your decarbonization strategies and monetize the benefits of owned land and climate mitigation.

Carbon Advisory Services

From rigorous carbon accounting and development of your carbon neutrality strategy to strategic carbon credit sourcing, we've got you covered.

Brokerage and trading

Access to carbon registries and custody services, B2B, OTC and exchange transactions, as well as clearing and execution services for the carbon market.

Financial solutions

Project finance, assets monetization and access to funding – we can help you monetize the benefits of climate mitigation.

Project development

We can help you at every stage of your emission-reduction project, including identification, feasibility, eligibility, registration and commercialization.

Why use Third Wave for carbon management initiatives?

Since the development of multiple exchange-traded platforms, Third Wave has helped clients manage risk in many asset classes. This is no different when it comes to carbon. We help institutional investors use climate mitigation investments as a cost-effective way to meet ESG commitments and mitigate climate risk.

We provide access and facilitate physical delivery of carbon credits and emission allowances at major carbon registries globally.

We hold memberships and facilitate customer clearing on all the major carbon and renewable energy exchanges.

We’ve guided multiple clients through the process of taking and making delivery of physical carbon credits and emissions allowances.

Zero Emissions Business Eco-System

Vertically Integrated Circularly Encompassing

Made In The USA Supply Chain Materials

Green concrete is an environmentally friendly alternative to traditional concrete, offering a sustainable solution for the construction industry. It is made by incorporating waste materials, such as fly ash or ground glass, in its production process, reducing the need for raw materials and decreasing carbon emissions.

Green concrete is an environmentally friendly alternative to traditional concrete, offering a sustainable solution for the construction industry. It is made by incorporating waste materials, such as fly ash or ground glass, in its production process, reducing the need for raw materials and decreasing carbon emissions.

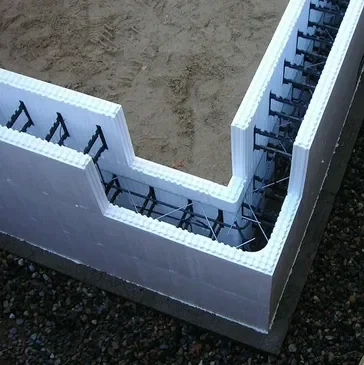

Insulating Concrete Forms (ICFs) are Expanded Polystyrene (EPS) panels joined with a web and tie system that take the place of traditional concrete forms with an added benefit – they stay in place. As the ICF forms are stacked to match the wall dimensions, they are reinforced with steel rebar, and then filled with concrete. The result is a building envelope of superior energy performance, unmatched comfort, and enduring strength. The permanence of concrete construction coupled with the energy efficiency of the ICF forms increases the value of your investment.

Insulating Concrete Forms (ICFs) are Expanded Polystyrene (EPS) panels joined with a web and tie system that take the place of traditional concrete forms with an added benefit – they stay in place. As the ICF forms are stacked to match the wall dimensions, they are reinforced with steel rebar, and then filled with concrete. The result is a building envelope of superior energy performance, unmatched comfort, and enduring strength. The permanence of concrete construction coupled with the energy efficiency of the ICF forms increases the value of your investment.

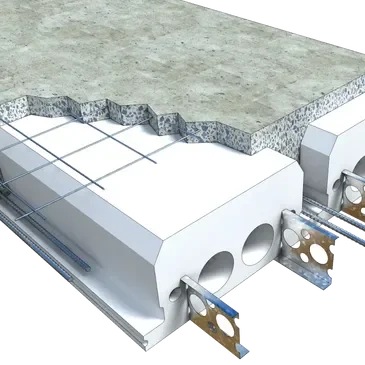

CelDeck® high density expanded polystyrene (HD-EPS) insulation is a rigid, foamed plastic with resilient closed cells molded in a range of densities and sizes to meet your application and specification requirements. Our HD-EPS is produced with modified bead provides all of the characteristics required for long-term performance: permanent R-Value, inherent water resistance, excellent physical strength, and dimensional stability. Contains No CFC, HCFC or HFC.

CelDeck® high density expanded polystyrene (HD-EPS) insulation is a rigid, foamed plastic with resilient closed cells molded in a range of densities and sizes to meet your application and specification requirements. Our HD-EPS is produced with modified bead provides all of the characteristics required for long-term performance: permanent R-Value, inherent water resistance, excellent physical strength, and dimensional stability. Contains No CFC, HCFC or HFC.

Book a Strategy Session

Lock in 30 minutes with a sustainability strategist. Unleash salient insights that lead to immediate wins.

Why We Exist

We empower organizations to unleash sustainable dominance. Our strategies cut waste, boost profit, and fuel growth.

Ready to Transform?

Send your project details. Let’s crush your sustainability goals together.